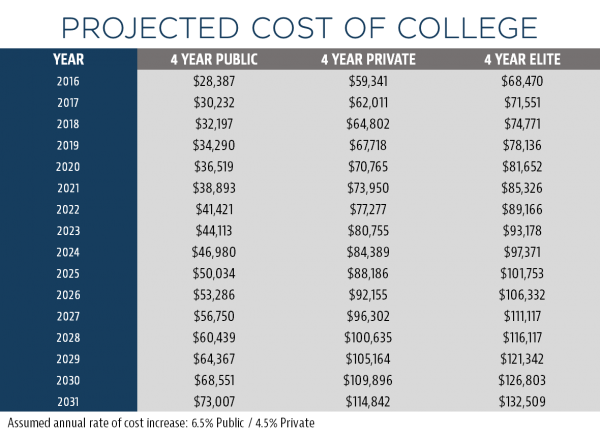

We all want what’s best for our children’s futures – for many families, that makes college planning and planning for college costs a top priority. However, quality higher education is coming at a premium these days, and all of the projections indicate that the trend will certainly continue in the coming years. Get started with your college planning NOW.

Planning for College Costs

When faced with these numbers, it becomes more important than ever to make sure that you’re taking the proper steps to maximize the growth potential of your children’s college fund, while also protecting it against loss and taxation. But how much needs to be saved to ensure that your prospective college graduate won’t be saddled with crippling student loan debt by the time they earn their degree? What are the best, most effective vehicles for accumulating the largest fund possible? What tax-favored strategies are out there that can be utilized to maximize the purchasing power of those savings?

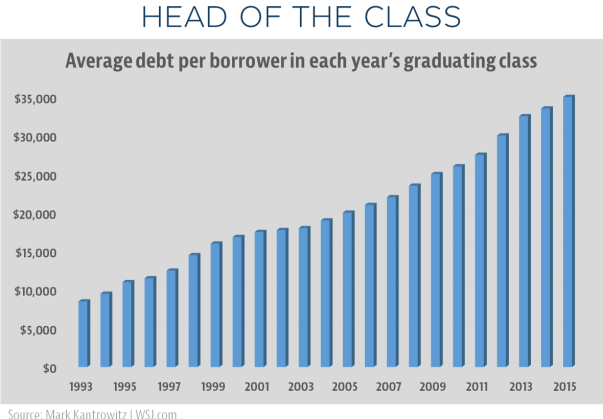

As a result, student loan debt continues to climb at a steady rate. (Outpacing even credit card debt!):